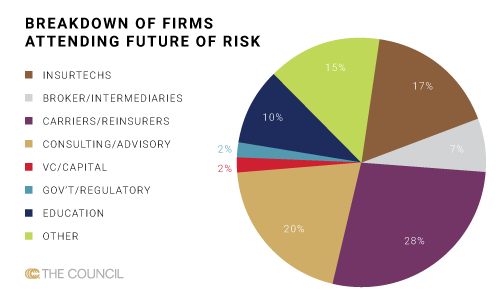

Here in Chicago, more than 200 insurtechs, brokers, carriers, students, consultants and venture capitalists are gathering to discuss how emerging technology can enable business processes, while at the same time evolving the inherent nature of risk. From the internet of things (IoT) and telematics, to blockchain and artificial intelligence (AI), the transfer of real-time data can be used to mitigate risk and drastically cut costs across the insurance value chain.

Here in Chicago, more than 200 insurtechs, brokers, carriers, students, consultants and venture capitalists are gathering to discuss how emerging technology can enable business processes, while at the same time evolving the inherent nature of risk. From the internet of things (IoT) and telematics, to blockchain and artificial intelligence (AI), the transfer of real-time data can be used to mitigate risk and drastically cut costs across the insurance value chain.

But as a wise man once said, with great power comes great responsibility. While technology presents itself as a ripe opportunity for brokers and risk managers, a constantly evolving risk landscape lacking sufficient historical data can be a very difficult risk to insure, at least for profit.

In a world that’s rapidly changing, insurers and brokers alike need to understand modern risk and how to adapt to a changing industry.

What We’re Hearing

One of the most noteworthy discussions we heard centered on the role of new college grads in an industry that is becoming increasingly technology dependent. Many agreed that students, who have grown up in a tech-driven and interconnected world, will play a crucial part in the industry’s adoption of and adaptation to technology. However, the job opportunities discussed were solely focused on the carrier and insurtech sectors. This was not so much an effort to exclude brokerages but likely due to the proportion of carrier-focused insurtechs at the conference.

Here are some additional noteworthy comments we heard on site:

”As the world economy grows, we’ll need a new AIG every year to cover the trillions of dollars of new risks.”

| – J. Patrick Gallagher, Chairman, President, & CEO, Arthur J. Gallagher & Co., on how the growing global economy requires more capital to transfer risk |

“90 % of all the data we’ve collected has been collected in the past two years. If you ask that same question two years from now, we’ll be able to say the same.”

| – Pete Miller, CEO, The Institutes, on the abundance of data and its role in the insurance industry |

“Companies are increasing their spend in risk management, but risk management academic departments are downsizing/decreasing,” findings from talent gap survey results.”

| – Phil Renaud, Executive Director, The Risk Institute, part of The Ohio State University Fisher College of Business |

“AI is not magic; it’s math, and AI can do the dirty work much faster and much cheaper”

| – Phil Alampi, Vice President of Marketing, DataCubes |

“We’ll see tremendous change in how we do it, but the essence of what we do stays the same… We take people’s risk.”

| – J. Patrick Gallagher, Chairman, President, & CEO, Arthur J. Gallagher & Co, on the evolution of risk transfer |

“In 2018, the global cost of cybercrime exceeded $1 trillion for the first time; 43 % of cyberattacks target small and midsized businesses; and more than 52 % of small businesses that suffered a cyberattack in 2018 went out of business by January 2019.”

| – Stephen Soble, CEO, Assured Enterprises, on the dangers of cyber crime |